How Much Lower Can We Go For Treasuries?

A long-awaited change to the US banking system is getting more plausible. Why is that so important for the Treasury market?

There are three magic letters which can make some US banks anxious. The S-L-R, or the supplementary leverage ratio, that US lenders have to comply with. Given that I covered the topic extensively once in the past, I won’t repeat myself and delve into the details. Therefore, if you’re not familiar enough with the SLR, please visit this article so that you’re able to get the gist.

For your convenience, I just want to briefly mention that the SLR is one of the capital ratios imposed by the Federal Reserve on lenders operating in the US. As each capital ratio, the SLR also requires banks to set aside some capital against assets they hold. What’s the most crucial about the SLR - this gauge isn’t risk-weighted, thus both risk-free reserves and risky corporate bonds are treated in the same way. With this in mind, we can move forward.

Trump wants lower yields

Yes, as literally every topic touches on Trump these days, it’s not going to be different with the SLR either. Namely, one of the goals for the US administration, as we knew some time ago, is to lower Treasury yields. Specifically, Trump has targeted the 10Y point in the curve. Why is that? First, the 10Y note is a lynchpin for global financial markets. Second, it’s also tied to consumer borrowing costs and, which is even more important, to mortgage rates. On top of that, Trump probably knows that he cannot do much with short-term rates as they’re chiefly driven by the Fed’s action, or lack thereof.

To achieve this objective, we need to be aware which elements Treasury bond yields are composed of. The simplest decomposition is: a swap rate and an additional premium on top of the swap rate. The first element is primarily driven by inflation expectations and related central bank policy. The second component has more to do with fiscal policy and banking regulation. We’ll focus on the latter.

Comprehensive SLR review?

That’s what some market participants seem to be betting on since Trump’s comments went viral. US banks have been pushing the Federal Reserve for long time to make some changes to the SLR. Its prevailing form includes both reserves and Treasuries, which can be burdensome, at least for some domestic lenders. This is because of the ample regime system and fiscal largesse we’re living in. These conditions mean more Treasury issuance, which undoubtedly needs to be purchased by someone. If the Fed isn’t an active buyer anymore, it’s actually offloading Treasuries from its balance sheet, other actors need to play their role. Since US banks are the largest creditor of the US govt, it shouldn’t be surprising that their voice cannot fall on deaf ears.

However, the US govt isn’t in charge of managing the SLR, only the Fed can implement such a shift after conducting some review. How to convince the Fed to do so? The US govt can argue that keeping the SLR unchanged could undermine a banks’ role in providing liquidity to market participants, and thereby preserving smooth market functioning.

Moreover, this task doesn’t necessarily need to be tough, given the fact that even the Fed itself arrived at a conclusion that “the SLR has been the most binding capital requirement for several large primary dealers in recent years. The SLR is particularly relevant for Treasury market intermediation as it has the potential to impose a high regulatory capital requirement for a relatively low-risk but high-volume activity.”1 Meanwhile, it’s a cliche that neither regulator would like to see a banking system struggling to fulfill its role in providing support for the financial system.

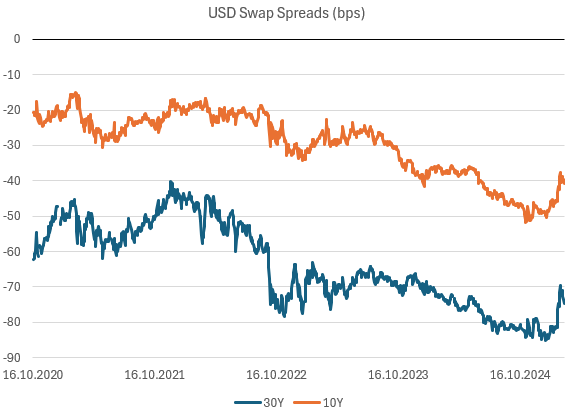

Markets listen to Trump carefully

Bets on a possible change to the SLR have risen lately, as evidenced by widening swap spreads - the difference between swap rates and Treasury yields. If I may have my cost of owning Treasuries lowered, I can afford to pay more for them. That’s a possible line of thinking. Why is that?

Let’s consider a simple example. If I’m a bank seeking a way to invest in Treasuries, I have two options. The first one is to simply purchase Treasuries, increase my balance sheet, and allocate an adequate amount of capital against this position. It’s a capital-consuming option. The second one is much less capital-consuming, as the bank can always establish a swap receive position in order to obtain exposure to lower interest rates (or rather hedge its other assets like loans). Notice that as a fixed-rate receiver in the swap agreement, I pay a floating rate and earn a fixed rate, effectively having exposure to lower rates.

What will happen with swap rates when everybody does the same (open receive positions)? You’re right, the price will go higher (relative to Treasuries), and that’s exactly what we’ve seen since late 2021 until the beginning of this year. Thus, if the Fed truly changes the SLR by permanently excluding reserves and cutting the amount of capital banks need to hold against Treasuries, it might push swap spreads even higher. In other words, Treasury yields could lower more than swap rates, which is what Trump would like to see.

Why not remove the SLR altogether? If you lower some capital ratios, or actually get rid of them, on the one side you increase banks’ ability to preserve proper market functioning, but on the other side you also lower the resilience of the banking system. Note that the SLR was introduced in the aftermath of the GFC crisis, thus you cannot throw the baby out with the bath water. Any adjustments to the SLR need to be made wisely after a thorough review. While there’s no doubt that reserves are fully risk-free, the same isn’t true for Treasuries all the time, as I wrote about a year ago.

Bond investors cheer

What does all this mean for longer-dated Treasuries? Any changes to the SLR, which will take some capital burden off banks, are positive for Treasuries, as banks would be able to take in more of them. Apart of the SLR, there are two additional factors that could drive demand for longer-dated Treasuries in the near term.

Firstly, US Treasury Secretary Bessent has suggested that a shift to longer-term issuance is a long way off2. Instead, he wants to see what the market demands and adjust a composition of issuance accordingly. Secondly, the latest Fed’s account from its January meeting showed that some officials mulled a possible pause of slowdown of the Fed’s balance sheet unwinding due to uncertainty with regards to “debt ceiling dynamics”. Putting it all together, the near-term outlook for longer-dated Treasuries presents an interesting picture.

Did you enjoy the piece? Please share this post and help me reach out to an ever-growing audience.

Would you like to share your opinion on the subject? Don't hesitate to leave a comment.

https://www.federalreserve.gov/econres/notes/feds-notes/assessment-of-dealer-capacity-to-intermediate-in-treasury-and-agency-mbs-markets-20241022.html#:~:text=The%20SLR%20has%20been%20the,risk%20but%20high%2Dvolume%20activity

https://www.reuters.com/world/us-treasurys-bessent-says-russia-could-win-sanctions-relief-war-talks-2025-02-20/